Your Bullsh*t-Free Guide to Income Tax in the UK

If you work in the UK, it's likely you'll pay income tax through the PAYE (Pay As You Earn) system, unless you're self-employed.

Your employer uses the UK PAYE system to withhold income tax and national insurance contributions from your wages and pays these deductions directly to HMRC (HM Revenue & Customs).

1. What will I pay income tax on in the UK?

You'll pay tax on various types of income when you work in the UK.

Factors such as how much you earn and whether you're resident or non-resident for tax purposes will also affect what you’ll pay tax on.

Download your FREE UK Tax Guide

UK residents for tax purposes normally pay tax on their worldwide income. However non-residents only pay tax on UK sourced personal income, interest in UK bank accounts, UK dividends, and UK rental income.

Types of income you'll pay tax on in the UK:

- Money you earn from employment

- Profits if you’re self-employed - including from services you sell through websites or apps

- Some state benefits

- Most pensions-including state pensions, company and personal pensions and retirement annuities

- Rental income (unless you’re a live-in landlord with income below the rent-a-room limit)

- Benefits you get from your job

- Income from a trust

Various sources of income are subject to taxation in the UK, reflecting the diverse financial landscapes individuals navigate.

You won’t pay tax on things like:

- The first £1,000 of self-employment income - this is your 'trading allowance'

- The first £1,000 of income from rented property (unless you use the Rent a Room Scheme)

- Dividends under your dividends allowance from company shares

- Some state benefits

- Premium bond or National Lottery wins

- Rent from a lodger in your house that’s below the rent-a-room limit

Exemptions from taxation encompass a range of earnings and windfalls, providing relief across various financial activities and endeavors.

Non-residents don’t usually pay UK tax on:

- State pension

- Interest from UK government securities (‘gilts’)

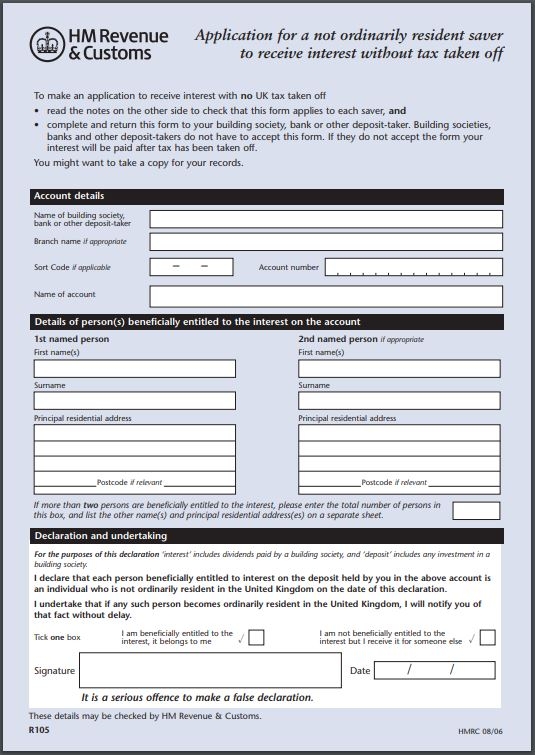

- Tax on savings interest, which is deducted by the bank or building society unless you give them a Form R105, pictured below:

How do I know if I'm UK resident for tax purposes or not?

If you moved to the UK, the Statutory Residence Test can help you determine whether you are resident or not, but you'll typically be taxed as a resident if you spend 183 days or more in the UK in a tax year.

These factors can also affect your status:

- Whether your home is in the UK or not

- If you work in the UK or abroad

- If you have family and other ties in the UK

- How long you spend in the UK

- Whether you've been resident in the UK in previous tax years

Taxback can help you with your non-resident UK tax return.

UK tax on state benefits

Your tax code can take account of taxable state benefits, so if you owe tax on them (for example, State Pension) it’s usually taken automatically from your other income.

If the State Pension is your only income, HM Revenue and Customs (HMRC) will write to you if you owe income tax and you may need to file a UK tax return.

Common state benefits that are taxable:

- State pension

- Jobseeker’s Allowance

- Carer’s Allowance

- Employment and Support Allowance (contribution based)

- Incapacity Benefit (from the 29th week)

- Bereavement Allowance

- Pensions paid by the Industrial Death Benefit scheme

- Widowed Parent’s Allowance

- Widow’s pension

Taxable state benefits form a comprehensive spectrum of financial support, reflecting the breadth of assistance provided within the UK's taxation framework.

Common tax-free state benefits

- Housing Benefit

- Employment and Support Allowance (income related)

- Income Support - though you may have to pay tax on Income Support if you’re involved in a strike

- Working Tax Credit

- Child Tax Credit

- Disability Living Allowance

- Child Benefit (income based - use the Child Benefit tax calculator to see if you’ll have to pay tax)

- Personal Independence Payment (PIP)

- Guardian’s Allowance

- Attendance Allowance

- Pension Credit

- Winter Fuel Payments and Christmas Bonus

- Free TV licence for over-75s

- Lump-sum bereavement payments

- Maternity Allowance

- Industrial Injuries Benefit

- Severe Disablement Allowance

- Universal Credit

- War Widow’s Pension

How much income tax will I pay in the UK?

How much income tax you pay in each tax year (the current tax year is from 6 April 2021 to 5 April 2022) depends on:

- How much of your income is above your Personal Allowance

- How much of your income falls within each tax band

The Standard Personal Allowance is £12,570, which is the amount of income you can earn without having to pay tax in the UK.

Standard Personal Allowance Rates:

| Allowances | 2022 to 2023 | 2021 to 2022 | 2020 to 2021 | 2019 to 2020 | 2018 to 2019 | 2017 to 2018 |

|---|---|---|---|---|---|---|

| Personal Allowance | £12,570 | £12,570 | £12,500 | £12,500 | £11,850 | £11,500 |

|

Income Limit for Personal Allowance |

£100,000 | £100,000 | £100,000 | £100,000 | £100,000 | £100,000 |

*The Personal Allowance goes down by £1 for every £2 of income above the £100,000 limit. You don’t get a Personal Allowance on taxable income over £125,140.

Your Personal Allowance also may be bigger if you claim Marriage or Blind Person’s Allowance.

Income Tax Rates and Bands

|

Tax rate |

Taxable income above your Personal Allowance for 2022 to 2023 |

|---|---|

|

Personal Allowance |

£0 to £12,570 |

|

Basic rate 20% |

up to £37,700 |

|

Higher rate 40% |

£37,701 to £150,000 |

|

Additional rate 45% |

over £150,000 |

*You don't get a Personal Allowance оn taxable income over £125,140.

**Income tax bands are different if you live in Scotland.

You'll also pay National Insurance Contributions if you’re 16 or over and either:

- Earn above £242 a week

- Are self-employed and making a profit of £11,908 or more a year

These contributions qualify you for certain benefits including:

- Basic state pension

- Additional state pension

- New state pension

- Contribution based jobseeker’s allowance

- Contribution based employment and support allowance

- Maternity allowance

- Bereavement benefits

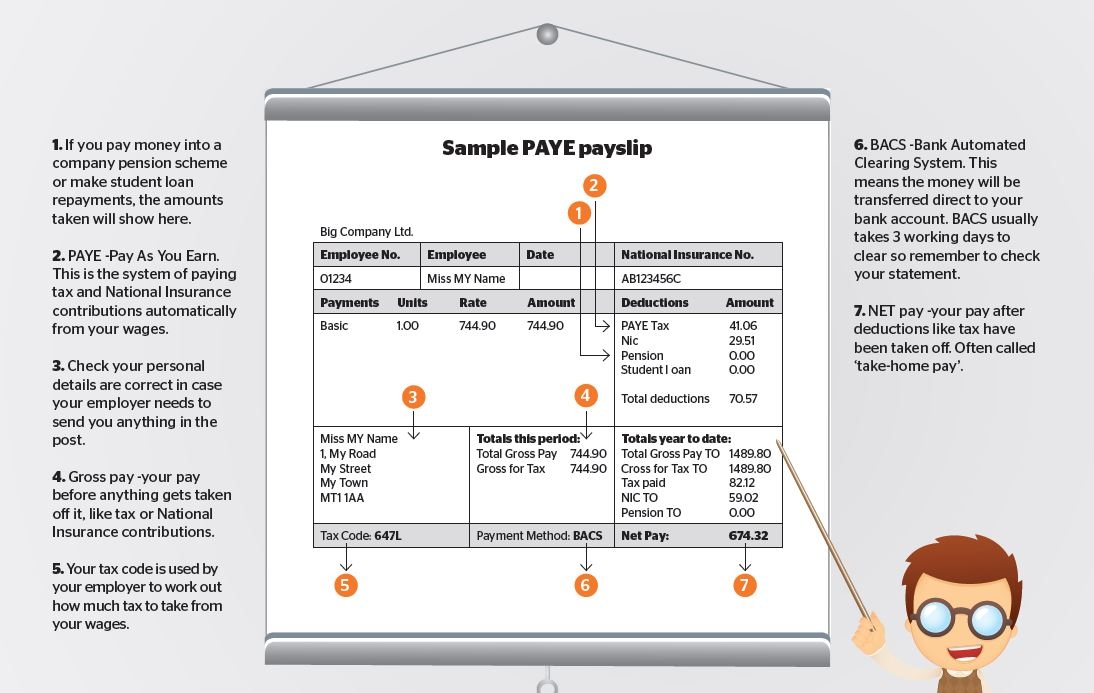

You'll need a National Insurance Number before you can start paying National Insurance contributions and you'll typically see this on your payslip and your P60. You can apply for a National Insurance Number directly from HMRC if you don’t have one.

Your employer will deduct national insurance contributions each time you're paid and you will see the amount on your payslip.

How much you pay depends on your employment status and income. As an employee, you'll pay Class 1 National Insurance contributions.

The National Insurance rates for most UK employees for the 2022 to 2023 tax year are:

| Your income |

Class 1 National Insurance rate |

|---|---|

| £190.01 - £967 | 13.25% |

| Over £967 a week | 2% |

You will contribute less if:

- You’re a married woman or widow with a valid ‘certificate of election’.

- You defer National Insurance because you’ve got more than one job.

If you're both employed AND do self-employed work, your employer will deduct your Class 1 National Insurance from your wages and you have to pay Class 2 and 4 payments for your self-employed work.

- Change your personal details (name, address, etc.)

- Or become self-employed

If you become unemployed or can’t work due to illness, you may be able to apply for National Insurance credits to fill any gaps in your contributions. ‘Cash in hand’ payments for work must be declared to HM Revenue and Customs (HMRC).

How do I know if I’m self-employed?

You’re probably self-employed if you:

- Run your own business and take responsibility for its success or failure

- Have several customers at the same time

- Can decide how, where and when you do your work

- Can hire other people at your own expense to help you or to do the work for you

- Provide the main equipment to do your work

- Are responsible for finishing any unsatisfactory work in your own time

- Charge an agreed fixed price for your work

- Sell goods or services to make a profit (including through websites or apps)

You can be both employed and self-employed, for example if you work for an employer during the day and run your own business at night.

Taxback can file your UK self assessment tax return for you and we will help you to minimise your tax liability.

If you’re a UK resident living abroad, you may be taxed on your income in the UK and the country you reside in. However, if the country you’re in has a double taxation agreement with the UK, you may not have to pay in both jurisdictions. Depending on this, you can apply for partial or full relief before you’re taxed or apply for a UK tax refund after you’ve been taxed.

To check if you are due any tax back, use our FREE tax refund calculator now!

2. Your UK Tax Code

One of the reasons you may be taxed incorrectly is if you’re using the wrong tax code. Your tax code appears on your payslip and is used by your employer to calculate exactly how much tax to take from your pay or pension. HMRC will tell them which code to use and it typically starts with a number and ends with a letter.

For example 1257L is the standard tax code for people who have one job or pension in the 2022/23 tax year.

UK Tax Code Letters Explained

| Letters | What they mean |

|---|---|

| L | You’re entitled to the standard tax-free Personal Allowance |

| M | Marriage Allowance: you’ve received a transfer of 10% of your partner’s Personal Allowance |

| N | Marriage Allowance: you’ve transferred 10% of your Personal Allowance to your partner |

| T | Your tax code includes other calculations to work out your Personal Allowance, for example it’s been reduced because your estimated annual income is more than £100,000 |

| 0T | Your Personal Allowance has been used up, or you’ve started a new job and your employer doesn’t have the details they need to give you a tax code |

| BR | All your income from this job or pension is taxed at the basic rate (usually used if you’ve got more than one job or pension) |

| D0 | All your income from this job or pension is taxed at the higher rate (usually used if you’ve got more than one job or pension) |

| D1 | All your income from this job or pension is taxed at the additional rate (usually used if you’ve got more than one job or pension) |

| NT | You’re not paying any tax on this income |

| S | Your income or pension is taxed using the rates in Scotland |

| S0T | Your Personal Allowance has been used up or you’ve started a new job and your employer doesn’t have the details they need to give you a tax code |

| SBR | All income from this job or pension is taxed at the basic rate in Scotland (usually used if you’ve got more than one job or pension) |

| SD0 | All income from this job or pension is taxed at the intermediate rate in Scotland (usually used if you’ve got more than one job or pension |

| SD1 | All income from this job or pension is taxed at the higher rate in Scotland (usually used if you’ve got more than one job or pension) |

| SD2 | All income from this job or pension is taxed at the top rate in Scotland (usually used if you’ve got more than one job or pension) |

Tax codes with ‘K’ at the beginning indicate that you have income that isn’t being taxed another way and it’s worth more than your tax-free allowance.

For most people, this happens when you’re:

● Paying tax you owe from a previous year from your wages or pension

● Getting benefits you need to pay tax on, such as state benefits or company benefits

Your employer or pension provider deducts the tax on the income that hasn’t been taxed from your wages or pension - even if another organisation is paying the untaxed income to you.

Employers and pension providers can’t take more than half your pre-tax wages or pension when using a K tax code.

Emergency Tax Codes

If your tax code has ‘W1’ or ‘M1’ at the end, then you’re on an emergency tax code and will pay tax on all your income above your personal allowance.

Your payslip will show:

● 1185 W1

● 1185 M1

● Or 1185 X

Reasons you may be on an emergency tax code:

● If you start a new job

● If you're working for an employer after being self-employed

● If you're getting company benefits or the State Pension

Once they have the correct details for you, your employer can update your tax code. HMRC will correct it automatically after you give your employer details of your previous income or pension.

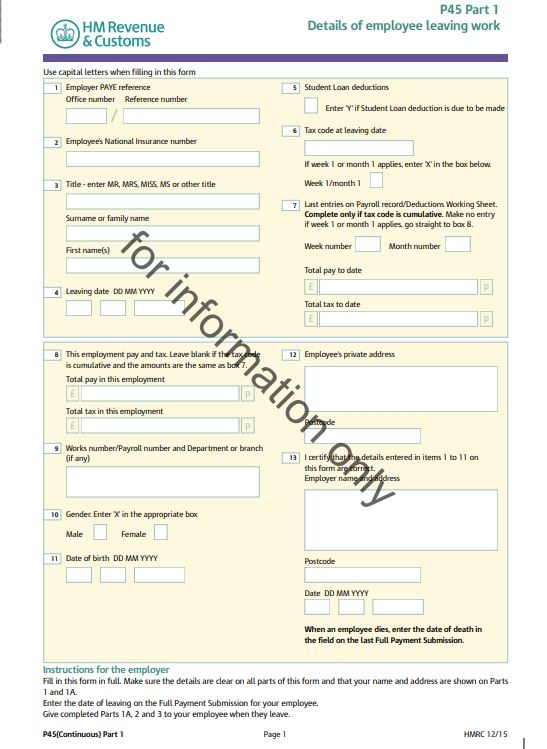

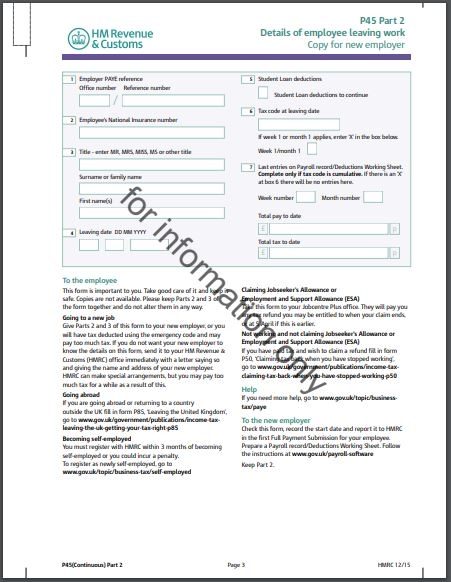

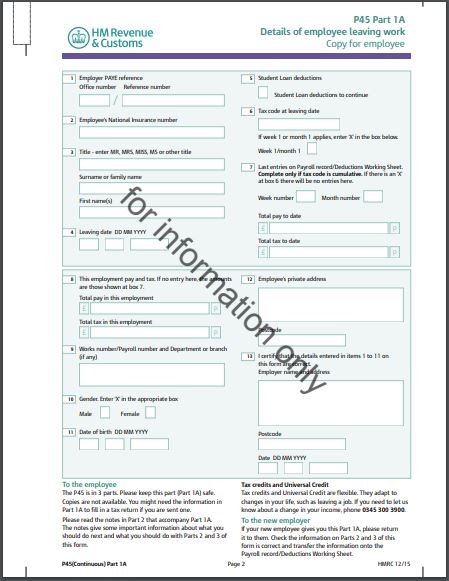

These details will come from your P45. You’ll get your P45 from your employer when you stop working for them and it will show how much tax you’ve paid in the tax year (6 April to 5 April).

Your P45 has 4 parts (Part 1, Part 1A, Part 2 and Part 3).

1. Your employer sends details for Part 1 to HMRC and gives you the other parts

2. You give Part 2 and 3 to your new employer (or Jobcentre Plus if you’re not working)

3. You keep Part 1A for your own records

By law your employer must give you a P45 when you leave the job. However, you won’t have a P45 if you’re starting your first job or you’re taking on a second job. In this case, your employer will need to work out how much tax you should be paying on your salary. They may use a ‘Starter Checklist’ to collect the information or may collect it another way.

The Starter Checklist has questions about any other jobs, benefits or student loans you have. It helps your employer work out your correct tax code before your first payday.

Your payslip shows your earnings before and after deductions, such as income tax and national insurance. You’ll get a payslip each time you’re paid either online or in a printed format and you can use these as proof of earnings, tax paid, and any pension contributions.

Your employer will provide you with a payslip unless you're:

- not an employee, e.g. a contractor or freelancer

- in the police service

- a merchant seaman

- a master or crew member working in share fishing (paid by a share in the profits or gross earnings of a fishing vessel)

Your payslip must be provided to you on or before payday.

Download your FREE UK Tax Guide

3. Income Tax Relief and Allowances in the UK

Tax relief and allowances reduce the amount of tax you need to pay.

‘Tax relief’ means:

- You pay less tax to take account of the cost of specific things like business expenses if you’re self-employed

- Or you get tax back or get it repaid in another way, like into a personal pension

TIP: Some reliefs are granted automatically - but others you must apply for. When you apply with Taxback, we’ll check for all applicable reliefs and allowances.

Tax relief applies to pension contributions, charity donations, maintenance payments, and time spent working on a ship outside the UK.

It also applies to work or business expenses – you may be able to:

- Get tax relief on what you spend running your business if you’re self-employed (a sole trader or partner in a partnership)

- Claim tax relief if you’re employed and you use your own money for travel and things you must buy for your job

Double Taxation Relief

If you're a non-resident working the UK, you could end up being taxed twice on your income in the UK and the country where you’re resident. This means you're taxed twice on the same income. However, you may be able to avail of a tax treaty so this doesn’t happen. A tax treaty can ensure:

- Partial or full relief before you’ve been taxed

- Or a UK tax refund

Each double-taxation agreement sets out:

- The country you pay tax in

- The country you apply for relief in

- How much tax relief you get

If the tax rates in the 2 countries are different, you’ll pay the higher rate of tax.

Countries with Double Taxation Agreements:

| Albania | Algeria | Anguilla | Antigua and Barbuda | Argentina | Armenia |

| Aruba | Australia | Austria | Azerbaijan | Bahrain | Bangladesh |

| Barbados | Belarus | Belgium | Belize | Bermuda | Bolivia |

| Bosnia-Herzegovina | Botswana | Brazil | British Virgin Islands | Brunei | Bulgaria |

| Burma | Cameroon | Canada | Cayman Islands | Chile | China |

| Colombia | Croatia | Cyprus | Czech Republic | Denmark | Egypt |

| Estonia | Ethiopia | Falkland Islands | Faroes | Fiji | Finland |

| France | Gambia | Georgia | Germany | Ghana | Gibraltar |

| Greece | Grenada | Guernsey | Guyana | Hong Kong | Hungary |

| Iceland | India | Indonesia | Iran | Ireland | Isle of Man |

| Israel | Italy | Ivory Coast | Jamaica | Japan | Jersey |

| Jordan | Kazakhstan | Kenya | Kiribati | Kosovo | Kuwait |

| Kyrgyzstan | Latvia | Lebanon | Lesotho | Liberia | Libya |

| Liechtenstein | Lithuania | Luxembourg | North Macedonia | Malawi | Malaysia |

| Malta | Marshall Islands | Mauritius | Mexico | Moldova | Monaco |

| Mongolia | Montenegro | Montserrat | Morocco | Namibia | Netherlands |

| Netherlands Antilles (Curacao, Sint Maarten and BES Islands) | New Zealand | Nigeria | Norway | Oman | Pakistan |

| Panama | Papua New Guinea | Philippines | Poland | Portugal | Qatar |

| Romania | Russia | Saint Kitts and Nevis | Saudi Arabia | Senegal | Serbia |

| Sierra Leone | Singapore | Slovak Republic | Slovenia | Solomon Islands | South Africa |

| South Korea | Spain | Sri Lanka | St Lucia | Sudan | Swaziland |

| Sweden | Switzerland | Taiwan | Tajikistan | Thailand | Trinidad and Tobago |

| Tunisia | Turkey | Turkmenistan | Turks and Caicos Islands | Tuvalu | Uganda |

| Ukraine | United Arab Emirates | Uruguay | USA | USSR | Uzbekistan |

| Venezuela | Vietnam | Zaire | Zambia | Zimbabwe |

*Double taxation agreements don’t apply to tax on gains from selling UK residential property.

Capital Gains Tax If You Live Abroad

If you live abroad, you only pay Capital Gains Tax if you make a gain on UK residential property. You won’t pay it on other UK assets, such as UK shares, and you won’t usually need to make a claim for assets you don’t pay tax on - but you should check the relevant double taxation agreement.

If you return to the UK after being non-resident, you may have to pay tax on any assets you owned before you left the UK - even if you’ve paid tax on any gains in the country you moved to. You can usually claim double-taxation relief.

Download your FREE UK Tax Guide

Tax Relief for Employees

If you use your own money for travel to clients for business or things that are essential for your job, you may be entitled to claim tax relief. You must have paid tax in the year you spent the money and how much you can claim depends on the rate you pay tax.

For example, if you spend £150 travelling to meet a client and you pay tax at a rate of 20%, then you can claim £30.

The rules for claiming tax relief in the UK are:

- You can only claim on items used for work that you don't use for personal purposes

- You can't claim relief on things you've spent money on where your employer has provided you with an alternative, for example if you bought a laptop but your employer has already given you one to use for work

- You need to keep records of what you spent and claim the relief within 4 years of the end of the tax year that you spent the money

- If your employer has paid for your expenses, you can't claim the relief

How to claim tax relief in the UK

How you can claim typically depends on how much you want to claim for:

Up to £2,500

You should make your claim:

- On a UK self-assessment tax return if you already file one

- With HMRC online or by posting form P87 if you don’t usually file a tax return

- By phone if you’ve had a successful claim in a previous year and your expenses are less than £1,000 (or £2,500 for professional fees and subscriptions)

- By applying with Taxback if you want to make it easy on yourself!

Over £2,500

- You can only claim using a self-assessment tax return

- You need to register if you don’t already fill one in

- You’ll get a letter telling you what to do next after you’ve registered

How you get tax relief

How you'll receive the relief also depends on how much you are claiming for.

Up to £2,500

If your claim is £2,500 or less for the tax year, HMRC will typically make adjustments through your tax code for the current tax year.

If you claim an estimated amount, HMRC will review it at the end of the tax year and make any adjustments through your tax code for the following year.

Claims over £2,500

If your claim is over £2,500 for the tax year, then you'll get the relief through your tax code for the current and next tax years, and receive a tax return to fill in.

They will also check your tax calculation for the previous year.

Uniforms, work clothing and tools

You may be able to claim tax relief on the cost of:

- Repairing/replacing small tools for your job like a pair of scissors or a drill

- Cleaning and repairing/replacing specialist clothing for your job

You can either claim:

- For what you spent, in this case you’ll need to keep receipts

- Or a ‘flat rate deduction’

Flat rate deductions are set amounts typically spent each year by employees in different occupations

| Industry | Occupation | Deduction £ |

|---|---|---|

| Agriculture | all workers | 100 |

| Airlines | pilots, co-pilots, helicopter pilots and uniformed flight deck crew | 1,022 |

| cabin crew - stewards and stewardesses |

720 | |

| Aluminium | a. continual casting operators, process operators, de-dimplers, driers, drill punchers, dross unloaders, firemen (engaged to light and maintain furnaces), furnace operators and their helpers, leaders, mould-men, pourers, remelt department labourers and roll flatteners | 140 |

| b. cable hands, case makers, labourers, mates, truck drivers and measurers and storekeepers | 80 | |

| c. apprentices | 60 | |

| d. all other workers | 120 | |

| Armed forces | all ranks in the: - Army - RAF - Royal Marines |

100 |

| Royal Navy | 80 | |

| Banks and building societies | uniformed doormen and messengers | 60 |

| Brass and copper | braziers, coppersmiths, finishers, fitters, moulders, turners and all other workers | 120 |

| Building | a. joiners and carpenters | 140 |

| b. cement works, roofing felt and asphalt labourers | 80 | |

| c. labourers and navvies | 60 | |

| d. all other workers | 120 | |

| Building materials | a. stone masons | 120 |

| b. tilemakers and labourers | 60 | |

| c. all other workers | 80 | |

| Clothing | a. lacemakers, hosiery bleachers, dyers, scourers and knitters, knitwear bleachers and dyers | 60 |

| b. all other workers | 60 | |

| Constructional engineering (includes buildings, shipyards, bridges and roads) | a. blacksmiths and their strikers, burners, caulkers, chippers, drillers, erectors, fitters, holders up, markers off, platers, riggers, riveters, rivet heaters, scaffolders, sheeters, template workers, turners and welders | 140 |

| b. banksmen, labourers, shop-helpers, slewers and straighteners | 80 | |

| c. apprentices and storekeepers | 60 | |

| d. all other workers | 100 | |

| Electrical and electricity supply | a. workers incurring laundry costs only | 60 |

| b. all other workers | 120 | |

| Trades ancillary to engineering | a. pattern makers | 140 |

| b. labourers, supervisory and unskilled workers | 80 | |

| c. apprentices and storekeepers | 60 | |

| d. motor mechanics in garage repair shop | 120 | |

| e. all other workers | 120 | |

| Fire service | uniformed fire fighters and fire officers | 80 |

| Food | all workers | 60 |

| Forestry | all workers | 100 |

| Glass | all workers | 80 |

| Healthcare staff in the National Health Service, private hospitals and nursing homes | a. ambulance staff on active service | 185 |

| b. nurses, midwives, chiropodists, dental nurses, occupational, speech, physiotherapists and other therapists, healthcare assistants, phlebotomists and radiographers shoes and stockings or tights allowance (where everyone is required to wear the same colour or style) |

125 12 shoes 6 tights or stockings |

|

| c. plaster room orderlies, hospital porters, ward clerks, sterile supply workers, hospital domestics and hospital catering staff | 125 | |

| d. laboratory staff, pharmacists and pharmacy assistants | 80 | |

| e. uniformed ancillary staff - maintenance workers, grounds staff, drivers, parking attendants and security guards, receptionists and other uniformed staff | 80 | |

| Heating | a. pipe fitters and plumbers | 120 |

| b. coverers, laggers, domestic glaziers, heating engineers and all their mates | 120 | |

| c. all gas workers and all other workers | 100 | |

| Iron mining | a. fillers, miners and underground workers | 120 |

| b. all other workers | 100 | |

| Iron and steel | a. day labourers, general labourers, stockmen, timekeepers, warehouse staff and weighmen | 80 |

| b. apprentices | 60 | |

| c. all other workers | 140 | |

| Leather | a. curriers (wet workers), fellmongering workers and tanning operatives (wet) | 80 |

| b. all other workers | 60 | |

| Particular engineering (work on commercial basis in a factory or workshop producing components such as wire, springs, nails and locks) | a. pattern makers | 140 |

| b. chainmakers, cleaners, galvanisers, tinners and wire drawers in the wire drawing industry and toolmakers in the lock making industry | 120 | |

| c. apprentices and storekeepers | 60 | |

| d. all other workers | 80 | |

| Police force | ranks of police officers up to and including chief inspector (but not West Yorkshire Police employees)

community support officers including Metropolitan Police (but not West Yorkshire Police employees)

|

140 |

| other police employees (but not special constables) | 60 | |

| Precious metals | all workers | 100 |

| Printing | a. letterpress section-electrical engineers (rotary presses), electrotypers, ink and roller makers, machine minders (rotary), maintenance engineers (rotary presses) and stereotypers | 140 |

| b. bench hands (periodical and bookbinding section), compositors (letterpress section), readers (letterpress section) telecommunications and electronic section wire room operators, warehousemen (paper box making section) | 60 | |

| c. all other workers | 100 | |

| Prisons | uniformed prison officers | 80 |

| Public service - socks and inland waterways | a. dockers, dredger drivers and hopper steerers | 80 |

| b. all other workers | 60 | |

| Public service - public transport | a. garage hands including cleaners | 80 |

| b. conductors and drivers | 60 | |

| Quarrying | all workers | 100 |

| Railways | See the appropriate category for craftsmen (for example engineers, vehicles) all other workers | 100 |

| Seamen | carpenters a. passenger liners |

165 |

| b. cargo vessels, tankers, coasters and ferries | 140 | |

| Shipyards | a. blacksmiths and their strikers, boilermakers, burners, carpenters, caulkers, drillers, furnacemen (platers) holders up, fitters, platers, plumbers, riveters, sheet iron workers, shipwrights, tubers and welders | 140 |

| b. labourers | 80 | |

| c. apprentices and storekeepers | 60 | |

| d. all other workers | 100 | |

| Textiles and textile printing | a. carders, carding engineers, overlookers and technicians in spinning mills | 120 |

| b. all other workers | 80 | |

| Vehicles | a. builders, railway vehicle repairers and railway wagon lifters | 140 |

| b. railway vehicle painters, letterers, and builders’ and repairers’ assistants | 80 | |

| c. all other workers | 60 | |

| Wood and furniture | a. carpenters, cabinetmakers, joiners, wood carvers and woodcutting machinists | 140 |

| b. artificial limb makers (other than in wood), organ builders and packaging case makers | 120 | |

| c. coopers not providing their own tools, labourers, polishers and upholsterers | 60 | |

| d. all other workers | 100 |

If your occupation isn’t listed, you may still be able to claim tax relief on a flat rate deduction of £60. For example, if you pay tax at a rate of 20% you could claim £12 tax relief on the £60 flat rate deduction.

You don’t need to keep records of what you’ve paid for if you claim a flat rate deduction.

Travel and overnight expenses

If you need to travel on business, to a place which is not your ordinary workplace, you may be entitled to claim tax relief on the cost of food or overnight expenses.

You can claim tax relief for money you’ve spent on things like:

- Public transport costs

- Hotel accommodation if you have to stay overnight

- Food and drink

- Congestion charges and tolls

- Parking fees

- Business phone calls and printing costs

Business mileage, fuel and electricity costs

You may also be able to claim tax relief on business mileage. Just note that you can’t claim for travelling from home/ accommodation to work and back, unless you’re travelling to a temporary place of work.

You may be able to claim tax relief on fuel or electricity you use for business and what you can claim for depends on whether you’re using your own or a company vehicle.

You can’t claim for travelling to and from your normal place of work, unless it’s a temporary place of work.

Using your own vehicle

If you use your own vehicle for business, you may be able to claim ‘Mileage Allowance Relief’. To work out how much tax relief you can claim, add up your business mileage for the tax year and multiply it by the approved mileage rates.

You can’t claim separately for:

- fuel

- electricity

- road tax

- MOTs

- repairs

To work out how much you can claim for each tax year you’ll need to:

- Keep records of dates and mileage or your work journeys

- Add up total mileage for each vehicle type you’ve used for work

- Subtract any amount your employer pays towards your costs, (sometimes called a ‘mileage allowance’)

Approved mileage rates from tax year 2022 to 2023

| First 10,000 business miles in a year | Each business mile over 10,000 in the tax year |

|---|---|

| 45p | 25p |

| 24p | 24p |

| 20p | 20p |

Passenger payments - cars and vans

5p per passenger per business mile for carrying fellow employees in a car or van on journeys which are also work journeys for them.

Only payments specifically for carrying passengers count and there is no relief if you receive less than 5p or nothing at all.

Using a company car for business

You can claim tax relief on the money you’ve spent on fuel and electricity for business trips in your company car. You must keep records to show the actual cost of the fuel.

If your employer reimburses part of the costs, you can claim relief on the difference.

Company cars

The charge is based on the price of the car for tax purposes (normally the list price) and accessories multiplied by an appropriate percentage based on the level of CO2 emissions and the fuel the car uses.

Car and Fuel Scale Benefits

| Car benefit | Percentage (see below) of list price Diesel | Percentage (see below) of list price Petrol |

|---|---|---|

| Fuel benefit | £25,300 | |

| CO2 emissions (g/km) | ||

| 0 - 50 | 17% | 13% |

| 51 - 75 | 20% | 16% |

| 76 - 94 | 23% | 19% |

| Each additional 5 | Further 1% | Further 1% |

| Diesel 160 and over/Petrol 180 and over | 37% | 37% |

Company vans

The charges are:

| Tax Year | Amount |

|---|---|

|

2022 to 2023 |

£3,600 |

| 2021 to 2022 | £3,500 |

| 2010 to 2021 | £3,490 |

| 2019 to 2020 | £3,430 |

| 2018 to 2019 | £3,350 |

Fuel charges - company cars and vans

Cars: To calculate the benefit charge on free or subsidised fuel for private use, the appropriate percentage used in calculating car benefit is applied to a set figure known as the car fuel benefit multiplier.

| Tax Year |

Amount |

|---|---|

| 2022 to 2023 | £25,300 |

| 2021 to 2022 | £24,600 |

| 2020 to 2021 | £24,500 |

| 2019 to 2020 | £24,100 |

| 2018 to 2019 | £23,400 |

The van fuel rates are:

| Tax Year |

Amount |

|---|---|

| 2022 to 2023 | £688 |

| 2021 to 2022 | £669 |

| 2020 to 2021 | £666 |

| 2019 to 2020 | £655 |

| 2018 to 2019 | £633 |

If your employer doesn’t pay you a mileage allowance, you can claim the full approved amount of Mileage Allowance Relief. However, if your employer pays a mileage allowance to you but it’s less than the approved amount, you can claim Mileage Allowance Relief on the difference.

If your employer pays you more than the approved amount you’ll have to pay tax on the difference. It’s important to keep records of the dates and mileage for each of your work journeys.

Using multiple vehicles

You can combine your business miles if you use more than one vehicle of the same type. If you use different types of vehicles, you should calculate them separately.

Using a company car for business

You can claim tax relief on the money you’ve spent on fuel or electricity for business trips in your company car. You should keep records to show the actual cost of the fuel or electricity you’ve bought or used.

If your employer reimburses only some of the money, you can claim relief on the difference.

Professional fees and subscriptions

You may be able to claim tax relief on fees or subscriptions you pay to approved professional organisations where the membership relates to your job.

You can’t claim tax back on fees or subscriptions for:

- Life membership subscriptio

- Fees or subscriptions you don't pay for yourself (e.g. if your employer has paid for them)

Your organisation can tell you how much tax you’re allowed to claim back.

Working from home in the UKProfessional fees and subscriptions

If you work from home in the UK on a regular basis or if you are required to work from home due to COVID-19, then you may be able to claim tax relief on some of the bills you pay.

You can’t claim tax relief if you choose to work from home. And any expenses should be related to your work, such as business telephone calls or the extra cost of gas and electricity for your work area.

You can’t claim for things you use for both private and business use, for example, rent or broadband access.

Your employer can pay you up to £6 a week to cover additional costs if you have to work from home and you don’t need to keep any records.

If you’ve agreed with your employer to work at home voluntarily or choose to work at home, you can’t claim tax relief on the bills you pay.

Other equipment

In many cases, you can claim tax relief on the full cost of ''substantial equipment''. Substantial equipment includes things like a computer you need for work because it qualifies for a type of capital allowance called annual investment allowance.

You can’t claim capital allowances for cars, motorcycles or bicycles you use for work, but you may be able to claim for business mileage and fuel costs.

You claim in a different way for small items that will last less than 2 years, such as uniforms and tools.

If your employer gives you money for the item then you can reduce the amount you claim tax relief on by the amount of money your employer gives you.

If your financial affairs are more complicated, you may need to pay income tax and National Insurance through self-assessment. In this case, you’ll need to file a yearly tax return. You must also fill in a tax return if your untaxed income is over £2,500, or contact the income tax helpline if it’s less than £2,500.

You can apply with Taxback for help with filing your self-assessed tax return.

Marriage Allowance

Marriage Allowance lets you transfer £1,260 of your Personal Allowance to your husband, wife or civil partner if they earn more than you. This reduces their tax by up to £252 in the tax year (6 April to 5 April of the next year).

To benefit as a couple, you must have an income of £12,570 or less and you can backdate your claim to include any tax year since 5 April 2018 that you were eligible for Marriage Allowance.

If your partner has died since 5 April 2018, you can still claim.

You can get Marriage Allowance if all of the following apply:

- You’re married/in a civil partnership

- You don’t earn anything/your income is £12,570 or less

- Your partner’s income is between £12,571 and £50,270 (or £43,662 if in Scotland)

It won’t affect your application for Marriage Allowance either of you are:

- Receiving a pension

- Living abroad - as long as you get a Personal Allowance

If you or your partner were born before 6 April 1935, then you might benefit more as a couple by applying for Married Couple’s Allowance instead.

You can’t get Marriage Allowance and Married Couple’s Allowance at the same time.

You can apply for Marriage Allowance online with HMRC and if successful, changes to your Personal Allowances will be backdated to the start of the tax year (6 April).

HMRC will give your partner their extra allowance either:

- By changing the tax code - this can take up to 2 months

- When they send their self-assessment tax return, if they’re self-employed

Your tax code will also change if you’re employed or get a pension and your new code will end with ‘N’.

If your circumstances change

Either of you can cancel your Marriage Allowance with HMRC and the date the allowance ends depends on who cancels it.

For example, if you stop transferring the allowance to your partner, it will run until the end of the tax year (5 April). But if your partner asks to stop receiving your allowance, they'll backdate the change to the start of the tax year you first started transferring it.

If you get divorced or dissolve your civil partnership, you can cancel the allowance online.

If you’re currently transferring your allowance to your partner you can choose to:

- keep transferring it until the end of the tax year (5 April)

- backdate the change to the start of the tax year (6 April)

If you ask to stop receiving your partner’s allowance, it will run until the end of the tax year.

If your income changes

You can contact Taxback and we can tell you if:

- Claiming Marriage Allowance will still benefit you

- Or you need to cancel your Marriage Allowance

If your partner dies after you’ve transferred some of your Personal Allowance to them:

- Their estate will be treated as having the increased Personal Allowance

- Your Personal Allowance will go back to the normal amount

If your partner transferred some of their Personal Allowance to you before they died:

- The Personal Allowance will remain at the higher level until the end of the tax year (5 April)

- Their estate will be treated as having the smaller amount

Savings and dividends allowances

You have tax-free allowances for both:

● savings interest

● dividends if you own shares in a company

You'll pay tax on any interest or dividends over your allowance.

4. Capital Gains Tax

Capital Gains Tax (CGT) Rates and annual tax-free allowances

CGT is a tax on the profit when you sell (or ‘dispose of’) an ‘asset’ that’s increased in value. It’s the gain you make that’s taxed, not the amount of money you receive. Some assets are tax-free and others you must pay tax on.

Every tax year, almost anyone who is liable to CGT gets an annual tax-free allowance. This is called the ‘Annual Exempt Amount’.

This means you don’t have to pay Capital Gains Tax if all your gains in a year are under your tax-free allowance.

You pay Capital Gains Tax on the gain when you sell (or ‘dispose of’):

● personal possessions worth £6,000 or more, excluding your car

● property that isn’t your main home

● your main home if you’ve let it out, used it for business or it’s very large

● shares that aren’t in an ISA or PEP

● business assets

These are known as ‘chargeable assets’. Depending on the asset, you may also be able to reduce any tax you pay by claiming a relief. If you dispose of an asset you jointly own with someone else, you have to pay Capital Gains Tax on your share of the gain. You only have to pay Capital Gains Tax on your total gains above an annual tax-free allowance.

You don’t pay Capital Gains Tax on certain assets, including any gains you make from:

● ISAs or PEPs

● UK government gilts and Premium Bonds

● betting, lottery or pools winnings

● gifts to your husband, wife, civil partner or a charity.

When someone dies

When you inherit an asset, Inheritance Tax is usually paid by the estate of the person who’s died. You only have to work out if you need to pay Capital Gains Tax if you later dispose of the asset.

Overseas assets

You may have to pay Capital Gains Tax even if your asset is overseas. There are special rules if you’re a UK resident but not ‘domiciled’ and claim the ‘remittance basis’.

If you’re abroad

You have to pay tax on gains you make on residential property in the UK even if you’re non-resident for tax purposes. You don’t pay Capital Gains Tax on other UK assets, e.g. shares in UK companies, unless you return to the UK within 5 years of leaving.

The annual tax-free allowance allows you to make a certain amount of gains every year before you have to pay tax. Nearly everyone who is liable to CGT gets this tax-free allowance.

There’s one Annual Exempt Amount for:

- most people who live in the UK

- executors or personal representatives of a deceased person’s estate

- trustees for disabled people (most other trustees get a lower Annual Exempt Amount)

Non-residents who disposed of a UK residential property will be liable to CGT and, in most cases, will be able to claim the Annual Exempt Amount in the same way as for UK residents.

However, this Annual Exempt Amount won’t be available to companies who dispose of a UK residential property as other allowances may be claimed.

Annual Exempt Amounts (AEA)

The AEA for the tax year 2023-2024 will be £6,000 for individuals and personal representatives, and £3,000 for the majority of trustees.

The AEA will be permanently fixed at £3,000 for individuals and personal representatives, and £1,500 for most trustees, for the tax year 2024-2025 and subsequent tax years.

The measure also limits the amount of CGT proceeds that can be reported to £50,000.

You can use your Annual Exempt Amount against the gains charged at the highest rates to minimise the tax you owe.

If you’re acting as an executor or personal representative for a deceased person’s estate, you may get the full Annual Exempt Amount during the ‘administration period’. This is typically the time it takes to settle the deceased person’s affairs and get a grant of probate (‘confirmation’ in Scotland). You’re entitled to the Annual Exempt Amount for the tax year in which the death occurred and the following 2 tax years. After that there’s no tax-free allowance against gains during the administration period.

If you’re acting as a trustee for a disabled person you use the higher Annual Exempt Amount above - and not the rate for ‘other trustees’. A disabled person in this context is a person who has mental health problems or receives the middle or higher rate of Attendance Allowance or Disability Living Allowance.

You won’t get the Annual Exempt Amount if you’re ‘non-domiciled’ in the UK and you’ve claimed the ‘remittance basis’ of taxation on your foreign income and gains. For example if you were born in another country and intend to return there, you may be ‘non-domiciled’.

You may have claimed the ‘remittance basis’ if you have income and gains from abroad and have decided that it’s beneficial to be taxed on the foreign income and gains that you bring into the UK, rather than on all income and gains that arise. Issues of domicile and tax on foreign gains are complicated and a lot depends on the facts. You can find out more by chatting to one of our friendly team members at Taxback.

UK Tax Rates for Capital Gains Tax

Discover the latest UK tax rates governing Capital Gains Tax, providing insights into the applicable rates for different asset types and income thresholds.

6 April 2017 onwards

- 10% and 20% tax rates for individuals (the tax rate you use depends on the total amount of your taxable income, so you need to work this out first)

- 18% and 28% tax rates for individuals for residential property and carried interest

- 20% for trustees or for personal representatives of someone who has died

- 28% for trustees or for personal representatives of someone who has died for disposal of residential property

- 10% for gains qualifying for Entrepreneurs’ Relief

- 28% for CGT on the property where the Annual Tax on Enveloped Dwellings is paid - the Annual Exempt Amount is not applicable

- 20% for companies (non-resident CGT on the disposal of a UK residential property)

1 in 3 people who pay tax in the UK is entitled to a tax rebate. There may be a number of reasons why you’re due a rebate from the UK, especially if you came to work there temporarily.

You may be able to get a tax refund in the UK (rebate) if you:

- Had too much tax taken from your pay

- Have stopped working

- Paid too much tax on pension payments

- Bought a life annuity

- If you used your own money for your job, for example, on fuel costs or work clothing

- Paid on savings interest if you’re on a low income

- Live in one country and have income in another - how you do this depends on whether you’re a UK resident with foreign income or a non-resident with UK income

It’s clear that many of us are missing out on reliefs and credits, resulting in an overpayment of tax, simply because we don't realise that we are owed this money! One of the easiest ways to find out exactly what you're owed from the last 4 years is to apply for a free, no-obligation refund estimate from our team at Taxback.

You can file a UK tax return with Taxback in three easy steps:

- Register with us here

- Send us your documents

- We do all the hard work involved in filing your return

Benefits of filing with Taxback

- Cost-effective & friendly tax return service

- Personal Tax Advisor

- Full compliance with the HMRC

- No complicated forms

- 24/7 Tax Help

- Free, no-obligation quote

Download your FREE UK Tax Guide

If you worked while you were backpacking in the UK, you could be due a tax refund. We can help you claim your tax rebate in the UK.

6. Frequently Asked Questions

Q. Do I need to file a UK tax return?

A. Most employees in the UK pay tax through their company’s payroll system and are not required to file a self-assessment tax return.

However there are a number of reasons why you may need to file a tax return including:

- You’re self-employed

- You’re in partnership or a company director

- You’re a higher rate taxpayer with annual income of £100,000 or more

- You have investment income of £10,000 or more

- You have capital gains in excess of the exempt amount (£12,300 for the 2021/22 tax year)

- You earned foreign income

- You have rental income

- You have a tax liability but no PAYE source of income

You should tell the HMRC if you think you need to file a tax return, however occasionally HMRC may issue a tax return for completion based on information from third parties (e.g. employers of expatriates).

If you are unsure whether you should file a tax return or not, you can contact Taxback.

Q. What if I leave my job?

A. If you leave your job your employer must give you a form called a P45. This is a document which shows your gross pay and the amount of the tax which was deducted at source from your pay during the tax year.It shows your:

- Tax code and the PAYE (Pay As You Earn) reference number of your employer

- National Insurance number

- Leaving date

- Earnings in the tax year

- How much tax was deducted from your earnings

Your employer will submit this information directly to HMRC on the last date that they pay you. If you don’t get a P45, you should request one from your employer and keep it safe, as you may need it to claim back any overpaid PAYE income tax. HMRC may not be able to refund any tax refund due without it.

It’s important to have a P45 if you start a new job. It may also help you if you want to claim a tax rebate.

Q. Can I claim a tax rebate if I leave the UK?

A. If you went to work in the UK for a number of years and returned to your home country, then chances are you’re due a UK tax rebate. You may be due a tax rebate for a number of reasons, including:

- You incurred work-related expenses

- You were short-term employed in the UK

- You didn’t work a full tax year

- Your position was made redundant

- You were on an emergency tax code

You can get a FREE, no-obligation estimate of your UK tax rebate by applying with Taxback here.

Claiming Your UK Tax Rebate

1 in 3 workers in the UK are due a tax rebate and the average refund is £963.

To apply for a UK tax rebate you will need either your P45 or P60 and details of any work-related expenses.

Applying with Taxback takes away all of the hassle and confusion and you’re guaranteed to receive your maximum refund as we’ll check for ALL applicable allowances and reliefs.

You can even use our UK tax rebate calculator to find out how much tax you are owed!

Simply follow these three steps to receive your tax refund the easy way:

- Apply with Taxback here

- We’ll tell you how much you’re owed from the last 4 years

- If you’re due a rebate, there are no upfront fees!

The average rebate with Taxback for people who have worked in the UK is £963 so don't leave this money behind!

Find out for free if you’re due a tax rebate by using our online UK tax calculator or apply here now to find out how much you could claim!

Get your UK tax rebate

7. Jargon Buster – Important UK Tax terms

Allowable Deductions

Any expenditure that can be deducted from gross income to reduce the amount subject to income tax before calculating how much tax is due.

Allowable Expenses

Expenses incurred purely for a trade, i.e. incurred ‘wholly and exclusively' for the purposes of the trade. Examples include cost of running vehicles, rent, repairs, and accountancy fees.

Assessable Income

The amount of money considered when calculating tax payments.

Asset

Something with value that you own outright or have an interest in (such as a leasehold).

In general, an asset must be:

- Apparatus used in carrying on a business

- Kept for permanent use in the business

- Functional in the context of a business, not part of the setting in which the business is carried on and not part of the building

Audit

Official inspection of your accounts.

Beneficiary

The individual who receives benefits from certain acts. For example, the beneficiary could be a person entitled to benefits from a trust property.

Benefit-in-Kind

Benefits-in-Kind are benefits employees or directors have that aren’t included in their salaries. They include things like company cars, private medical insurance or free accommodation.

Most benefits from employment provided in addition to your salary are subject to income tax.

Generally, there are two types of benefits that an employee may get in addition to a salary:

1. Benefits-in-kind - benefits that an employee receives that cannot be converted into cash but have a cash value. Examples include provision of accommodation or a company car, or loans given at a special rate.

2. Benefits (other than benefits-in-kind). Examples include vouchers, holidays, payment of an employee's bills and prizes.

Capital Gain

The profit from the sale of a capital asset. Examples include assets such as land, buildings, and shares.

Capital Gains Tax (CGT)

A type of tax levied on the profit from the disposal of a capital asset. Tax on gains that arise on the sale of capital assets, items such as land, buildings, and shares.

Corporate Income Tax

A type of tax levied on the income of corporations, usually imposed at the national level.

Creditor

Person or company to whom money is owed.

Deduction (tax)

A reduction in tax obligation from the taxpayer’s gross income. Deductions are removed from taxable income and thus lower tax liability.

Dependant

Individual who relies on another. For example a child or disabled family member.

Disposal

Selling, gifting or exchanging an asset.

Dividends

Sum of money regularly paid by a company to shareholders from its profits.

Domicile

Permanent home country of a person or the country they live in and have substantial ties with.

Double Taxation Treaty

An agreement with two or more countries to reduce how much tax a worker or company must pay, so they don’t pay tax twice on the same income.

Earned Income

Income derived from paid work.

Effective Tax Rate

Used to describe the average rate at which an individual or corporation is taxed on their taxable income.

Emergency Tax

The tax an individual pays when it’s not clear what tax band they should be assigned to. To avoid this, you should give your employer your P45.

Excise Tax/Duty

A tax on the sale of particular goods.

Flat Tax

A tax system with a constant marginal rate.

Gross Income / Pay

The amount of income paid to an employee before any deductions are made.

Income Tax

A tax levied directly on income.

Inheritance Tax

Inheritance Tax is a tax on the estate (the property, money and possessions) of someone who's died. There's normally no Inheritance Tax to pay if either:

- the value of your estate is below the £325,000 threshold

- you leave everything to your spouse or civil partner, a charity or a community amateur sports club.

Net Income

The total income after any deductions have been made.

PAY As You Earn (PAYE)

A system for paying income tax and other contributions.

PAYE Employee

Pay As You Earn is a tax system where the employer calculates and deducts the amount of tax due.

Payslip

A statement given to an employee detailing income earned and relevant deductions such as tax and national insurance.

Penalties

A tax penalty is sometimes imposed for an underpayment of tax or late filing.

Personal Allowance

Your tax-free Personal Allowance. The standard Personal Allowance is £12,570, which is the amount of income you don't have to pay tax on. Your Personal Allowance may be bigger if you claim Marriage Allowance or Blind Person's Allowance. It's smaller if your income is over £100,000.

P45

This is a certificate given to employees at the end of their employment with details of gross pay and tax paid for the year to date.

P60

This is a statement issued to employees at the end of a tax year detailing your income and tax paid. It’s important to keep this as it could help you apply for a potential tax refund. Your P60 shows the tax you’ve paid on your salary in the tax year (6 April to 5 April). You get a separate P60 for each of your jobs.

Progressive Tax

A tax where the rate increases as the taxable amount increases.

Qualifying exemptions for Capital Gains Tax (CGT)

There are a number of qualifying exemptions from Capital Gains Tax.

Rebate (of tax)

A refund or repayment of tax given to the taxpayer if the tax they owe is less than the amount of tax withheld or estimated tax they paid.

Self-Assessment

Calculation of your own tax liability, for example if you're self-employed you must file a tax return.

Stamp Duty Land Tax

You must pay Stamp Duty Land Tax (SDLT) if you buy a property or land over a certain price in England and Northern Ireland.

State Benefits

Benefits given by the government to assist people in certain circumstances, such as the unemployed, disabled or ill.

Starter Checklist

Tax

Tax is a compulsory contribution levied by the government on items such as employee’s income, business profits, and the cost of goods and services.

Tax Agent

A tax agent or tax preparer, like Taxback, prepares and files the returns of income on behalf of taxpayers.

Tax Authorities

The authority responsible for tax collection.

Taxation at Source

When tax is taken out of your income before it’s paid, e.g. by your employer.

Tax Credits

Tax credits are sums that can be offset against a tax liability.

Tax Evasion

Tax evasion is an illegal non-payment or underpayment of tax.

Taxable Income

Taxable income is the amount of income used to calculate an individual or company’s income tax.

Tax Pack

Information to assist taxpayers in completing their tax return.

Taxpayer

An individual who is liable to pay tax.

Tax Relief

Tax relief Reduces the amount of income tax due on earned income.

Tax Return

A tax return is a statement from a taxpayer to the tax authorities with details of income earned and personal circumstances.

Tax Threshold

The level of income at which an individual starts paying tax or a higher rate of tax.

Value Added Tax (VAT)

Value-Added Tax (VAT) is a tax on consumer spending. Most goods and services supplied in the UK are subject to VAT. Some things are exempt from VAT , eg postage stamps, financial and property transactions. The VAT rate businesses charge depends on their goods and services.

Withholding Tax

Tax deducted at source, for example by an employer.

YTD

‘YTD’ is often found on official documents such as payslips. It simply means year-to-date.

|

Allowances |

2022 to 2023 |

2021 to 2022 |

2020 to 2021 |

2019 to 2020 |

2018 to 2019 |

2017 to 2018 |

|

Personal Allowance |

£12,570 |

£12,570 |

£12,500 |

£12,500 |

£11,850 |

£11,500 |

|

Income limit for Personal Allowance |

£100,000 |

£100,000 |

£100,000 |

£100,000 |

£100,000 |

£100,000 |